“9 Mistakes Killing American Reshoring Deals Before They Ever Reach Your Shop Floor.”

“The work is coming back—but not to the shops still behaving like it’s 1998.”

This article breaks down how U.S. manufacturers lose reshoring opportunities by: underinvesting in automation, ignoring workforce training, relying on crumbling infrastructure, and failing to prove they can handle IP‑sensitive or final‑assembly work.

This article provides a sharp, timely reality in the reshoring landscape as of January 2026. With ongoing tariff pressures, policy incentives like the CHIPS Act extensions, and geopolitical shifts accelerating announcements of domestic manufacturing investments, work is returning to the U.S. — but many legacy facilities and smaller-to-mid-size manufacturers risk being bypassed because they haven’t modernized.

This article highlights how outdated practices — clinging to manual processes, minimal automation, stagnant workforce development, neglected infrastructure, and inability to demonstrate secure handling of intellectual property (IP) or complex final-assembly — cause OEMs and investors to look elsewhere (e.g., to greenfield sites, highly automated partners, or even nearshoring alternatives).

Fortune magazine recently posted and article: Despite Trump’s best efforts to reshore manufacturing, blue-collar employment is plunging for the first time since the pandemic with 59,000 lost jobs on Fortune (published November 25, 2025). That piece highlights a stark irony: Despite aggressive tariffs announced in April 2025, U.S. factory employment shed over 70,000 positions by early 2026, amid policy uncertainty and structural issues like skills gaps.

These factors explain why reshoring announcements often lead to new builds or FDI rather than revitalizing existing Midwest/Rust Belt shops — and why deals die before reaching the floor.

“9 Mistakes Killing American Reshoring Deals Before They Ever Reach Your Shop Floor” is a list that draws directly from 2025-2026 trends: persistent skills gaps (hundreds of thousands of unfilled roles), high costs without automation offsets, infrastructure delays, policy uncertainty, and failures in proving readiness for IP-sensitive or complex final-assembly work. Each mistake explains why OEMs walk away early in feasibility studies, site visits, or negotiations.

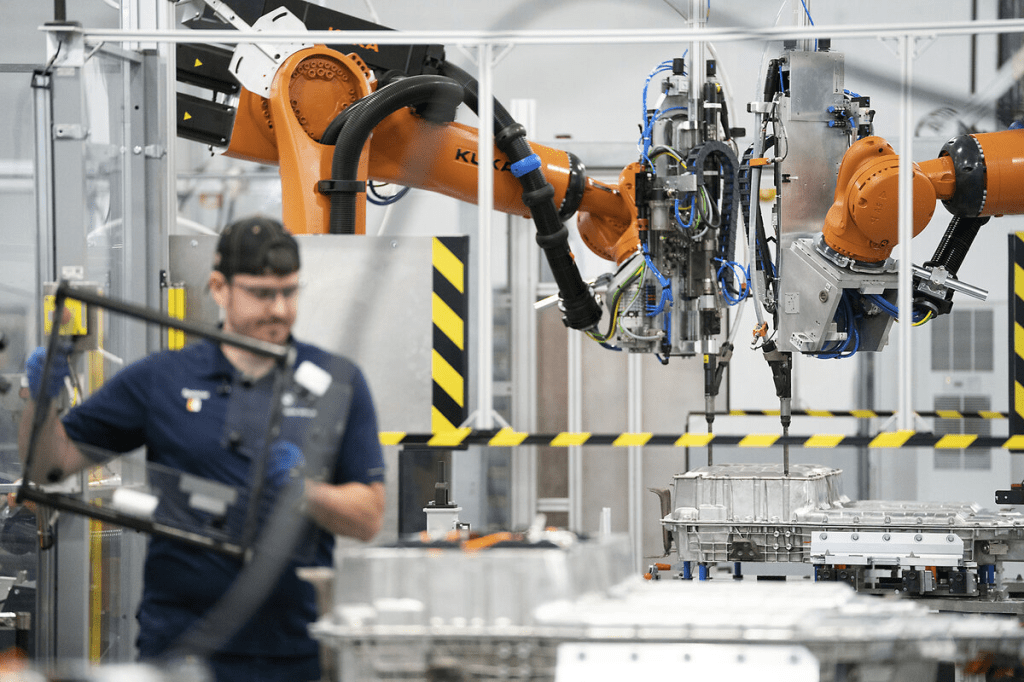

1. Clinging to Manual Processes Instead of Investing in Automation

Many shops rely on outdated manual lines from the 1990s-2000s era, ignoring robotics, AMRs, and AI-driven systems that offset U.S. labor costs ($25-30/hour vs. far lower abroad). Without heavy automation, total cost of ownership (TCO) calculations make reshoring unviable once subsidies fade. Result: Deals go to automated competitors or new builds.

Real-World Case Studies

Failure Case: Stanley Black & Decker’s Craftsman Tools Factory (Texas, ~2010s–early 2020s, with lessons persisting into 2025) Stanley Black & Decker invested ~$90 million in a highly automated factory in Fort Worth, Texas, to reshore production of mechanics’ tools from China. However, poor implementation led to major failures, showing why many legacy shops avoid or botch upgrades: They underestimate the expertise needed, resulting in deals collapsing before production starts.

Success Case: Keen Footwear’s Kentucky Factory (Opened June 2025) Keen Footwear reshored construction boot production to a new, highly automated plant in Shepherdsville, Kentucky. They invested in robotics: orange robotic arms load parts, automated systems fuse soles, producing a pair every 22 seconds with just ~24 employees. This made domestic production viable, cutting shipping times and responding to demand for “American Built” products.

2. Ignoring Workforce Upskilling and Training Programs

Legacy facilities often lack ongoing training in digital tools, robotics, predictive maintenance, or collaborative automation. With 409,000+ unfilled jobs in 2025 (and projections of 1.9 million at risk by 2033), OEMs prioritize partners with proven skilled teams. Ford’s struggle to fill high-pay mechanic roles exemplifies this — shops without upskilling programs get bypassed.

(Insert visuals here: Images showing the difference skilled, trained teams make in action.)

. Relying on Crumbling or Inadequate Infrastructure

Aging plants with unreliable power, limited space for expansion, outdated logistics, or insufficient energy capacity fail site assessments — especially for power-hungry high-tech ops like fabs or EV battery lines. Greenfield sites get the nod instead.

4. Failing to Demonstrate IP Protection and Cybersecurity Readiness

OEMs in semiconductors, aerospace, or defense demand robust cybersecurity, secure processes, and certifications. Shops without traceability, encrypted systems, or proven protocols for handling sensitive designs get eliminated early — reshoring often favors new facilities with built-in safeguards.

5. Underestimating Total Cost of Ownership (TCO) and Hidden Expenses

Many miscalculate by focusing only on labor, ignoring tariffs on inputs, redesign for U.S. automation, regulatory compliance, or supply chain rebuilding. This leads to unrealistic bids that collapse during due diligence.

6. Neglecting Supplier Ecosystem Rebuilding

Reshoring requires domestic suppliers for components — but many shops lack local networks, leading to imported dependencies and delays. OEMs avoid partners who can’t prove a mature, resilient ecosystem.

7. Overlooking Regulatory and Permitting Delays

Legacy sites often face slow permitting for upgrades or expansions, while new builds in incentive-friendly zones move faster. Policy uncertainty (e.g., tariff fluctuations) compounds hesitation.

8. Rushing Without Pilot Testing or Proof-of-Concept

Shops push full commitments without small-scale pilots to validate processes, quality, or scalability in a U.S. context — leading to early red flags in negotiations and lost trust.

9. Failing to Adapt Product/Process Design for U.S. Realities

Products designed for low-cost offshore labor often need redesign for automation, higher precision, or sustainability mandates. Shops that don’t proactively redesign or prove U.S.-optimized assembly lose out on final-assembly deals.

These nine mistakes explain the “jobless boom” paradox: Reshoring investments surge, but legacy shops miss the wave, contributing to net employment declines. The fix? Invest now in automation, training, infrastructure, and capability proofs — before the opportunity passes to more agile players. Shops that evolve beyond 1998 stand to capture the real reshoring gains in 2026 and beyond.

Leave a comment